Simulating Strategies

The Simulate tab in the Strategy Lab lets you test a strategy idea against historical data before committing real capital.

All computation runs in your browser - results appear instantly and you can adjust parameters and re-run as many times as you like.

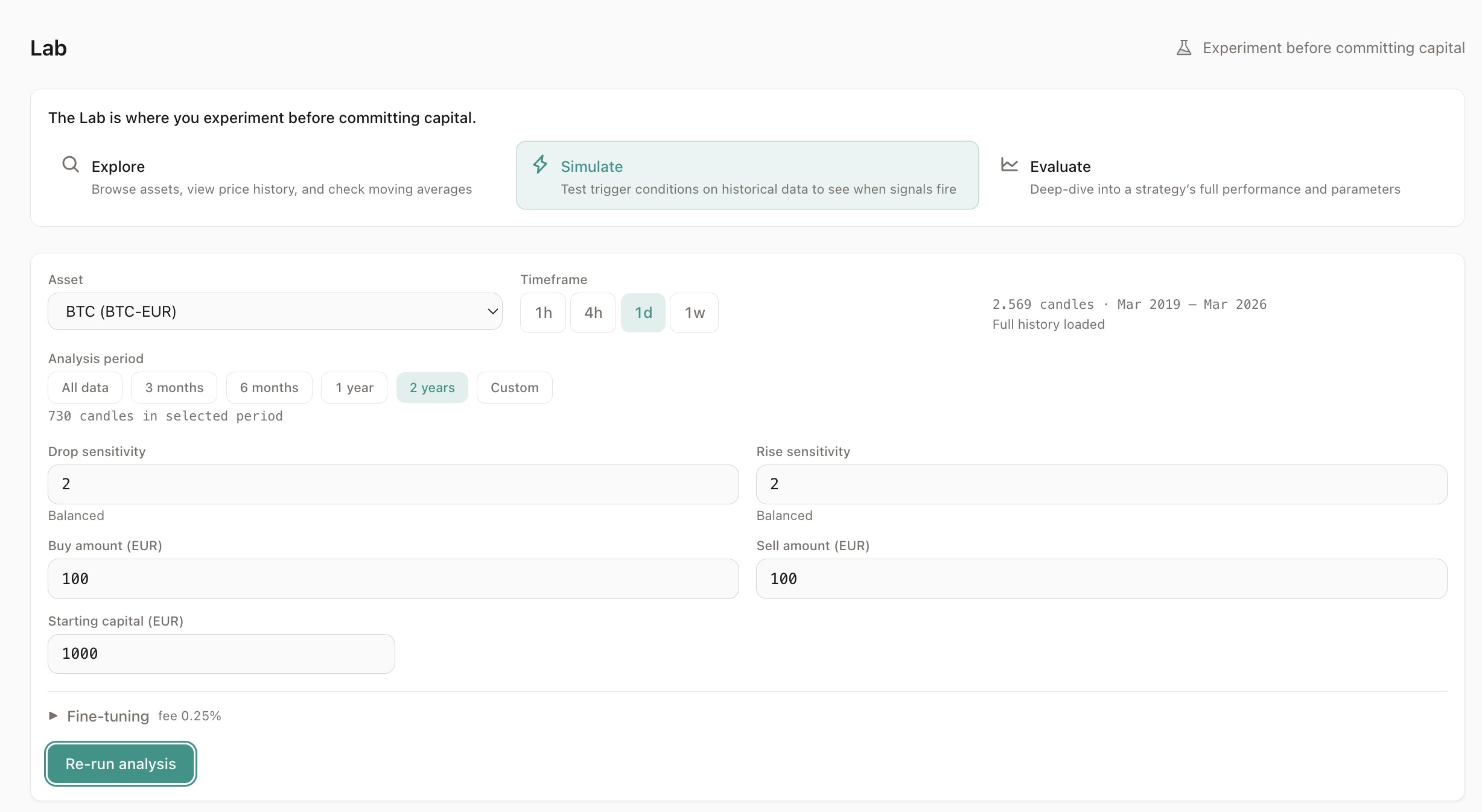

Setting Up a Simulation

Section titled “Setting Up a Simulation”Configure the following parameters:

| Parameter | What it controls |

|---|---|

| Asset | The trading pair to simulate (e.g. BTC-EUR) |

| Timeframe | Candle duration (1h, 4h, 1d) |

| Drop sensitivity | How much price must drop to trigger a buy (sigma) |

| Rise sensitivity | How much price must rise to trigger a sell (sigma) |

| Buy amount | EUR spent per buy order |

| Sell amount | EUR received per sell order |

| Starting capital | Total EUR allocated to the strategy |

| Fee % | Exchange fee per trade (default 0.25%) |

If you navigated from the Explore tab, the asset and timeframe are pre-filled.

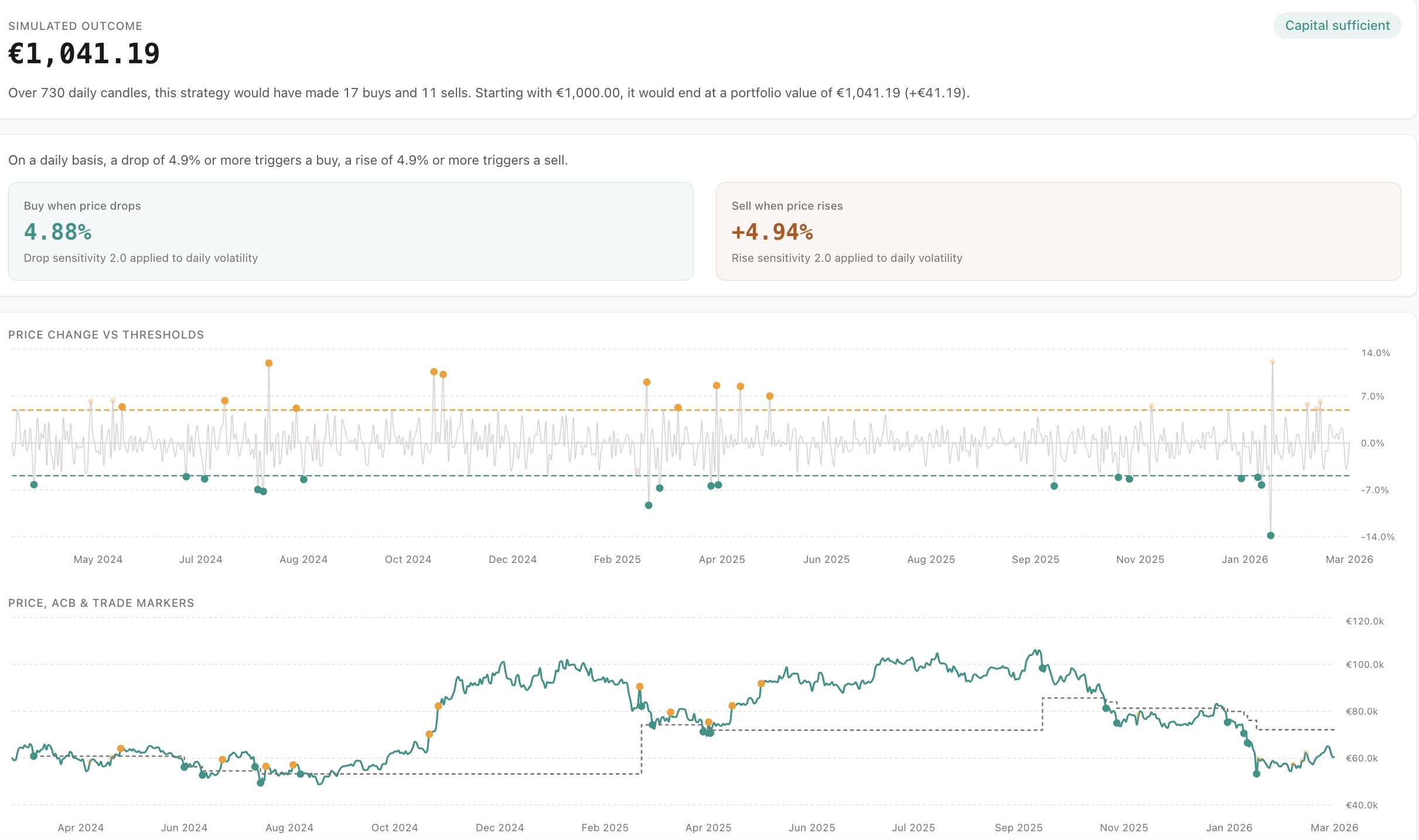

Reading the Results

Section titled “Reading the Results”Results appear in layers, from simple to detailed:

Verdict (top level)

Section titled “Verdict (top level)”The hero number: portfolio end value. This is the single most important number.

Below it:

- Capital safety badge: safe or insufficient

- Summary sentence: “Over 1,440 daily candles, this strategy would have made 10 buys and 5 sells.”

Computed Thresholds

Section titled “Computed Thresholds”Two boxes showing the calculated buy and sell thresholds:

- Buy threshold (e.g. -4.2%) - “A drop of 4.2% or more triggers a buy”

- Sell threshold (e.g. +6.1%) - “A rise of 6.1% or more triggers a sell”

These are derived from the sigma values and the asset’s historical volatility.

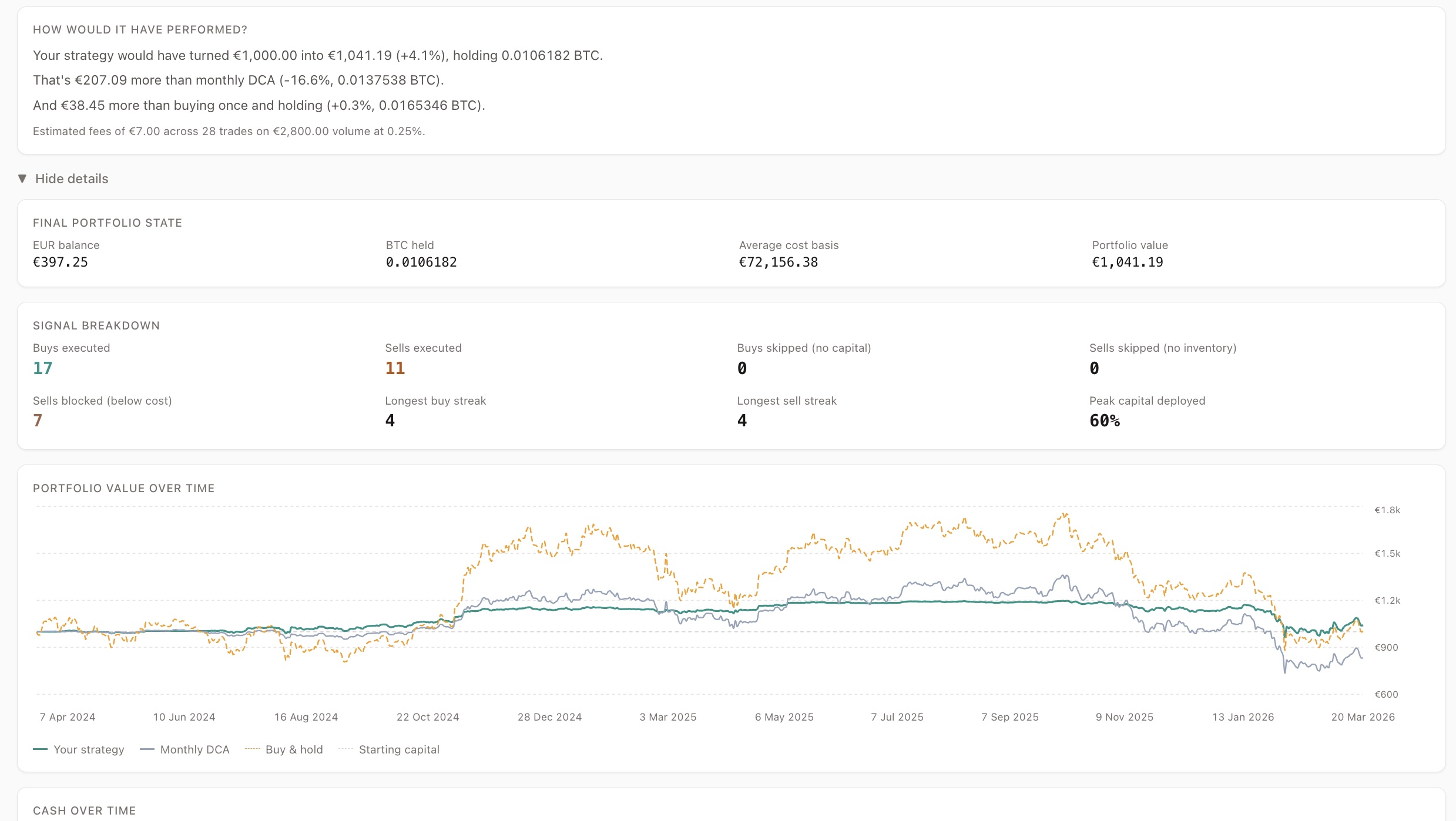

Performance Comparison

Section titled “Performance Comparison”Your strategy compared to two benchmarks:

- Monthly DCA - buying a fixed amount every month

- Buy and hold - buying once at the start

This shows whether the strategy’s active management adds or loses value compared to simpler approaches.

Fee impact is shown transparently.

Charts

Section titled “Charts”Two-panel chart:

- Top panel - candle-to-candle price change with buy/sell threshold lines

- Bottom panel - price chart with trade markers and ACB line

Trade markers:

- Solid dots - executed trades

- Faded dots - ignored trades (blocked by capital, ACB, or inventory rules)

Narrative

Section titled “Narrative”A “What happened” section that surfaces problems in plain language:

- Capital ran out during a buy cluster

- Sells were blocked because price was below ACB

- Inventory was insufficient for sell triggers

If everything looks healthy, you get a clean bill of health.

Expandable Details

Section titled “Expandable Details”For deeper analysis:

- Signal breakdown (how many buys/sells executed vs ignored)

- Portfolio state over time

- Equity curve (strategy vs DCA vs buy & hold)

- Cash-over-time chart with danger zone

Understanding Ignored Triggers

Section titled “Understanding Ignored Triggers”Not every signal results in a trade. The simulation shows exactly why:

Buy triggers ignored because:

Section titled “Buy triggers ignored because:”- Insufficient capital - allocated capital is fully deployed

- Signal clustering - multiple buy signals arrive faster than capital recycles

Sell triggers ignored because:

Section titled “Sell triggers ignored because:”- ACB protection - price is below the average cost base (Aurono never sells at a loss)

- No inventory - nothing to sell yet

Ignored triggers are not bugs - they are safety constraints working as designed.

Suggestions

Section titled “Suggestions”If the simulation reveals issues, suggestion cards appear:

- “Capital insufficient - try raising buy sigma to reduce trigger frequency”

- “Many sells blocked by ACB - try raising sell sigma for more patience”

- “Idle capital - try lowering buy sigma to deploy capital faster”

Click a suggestion to re-run instantly with adjusted parameters.

Creating a Strategy from Simulation

Section titled “Creating a Strategy from Simulation”When you are satisfied with the results, click “Create strategy”. This navigates to the strategy creation form with all parameters pre-filled:

- Symbol and timeframe

- Buy and sell amounts

- Allocated capital

- Computed drop and rise percentages

Key Principles

Section titled “Key Principles”- The simulation uses the same logic as Aurono’s live engine

- All computation runs client-side - no backend calls needed

- Results are deterministic - same parameters always produce the same outcome

- The tool answers: “Can this strategy survive its own rules?” - not “Will this make money?”